How OECD Pillar 2 Is Reshaping UAE's Tax Landscape: What Multinational Companies Need to Know

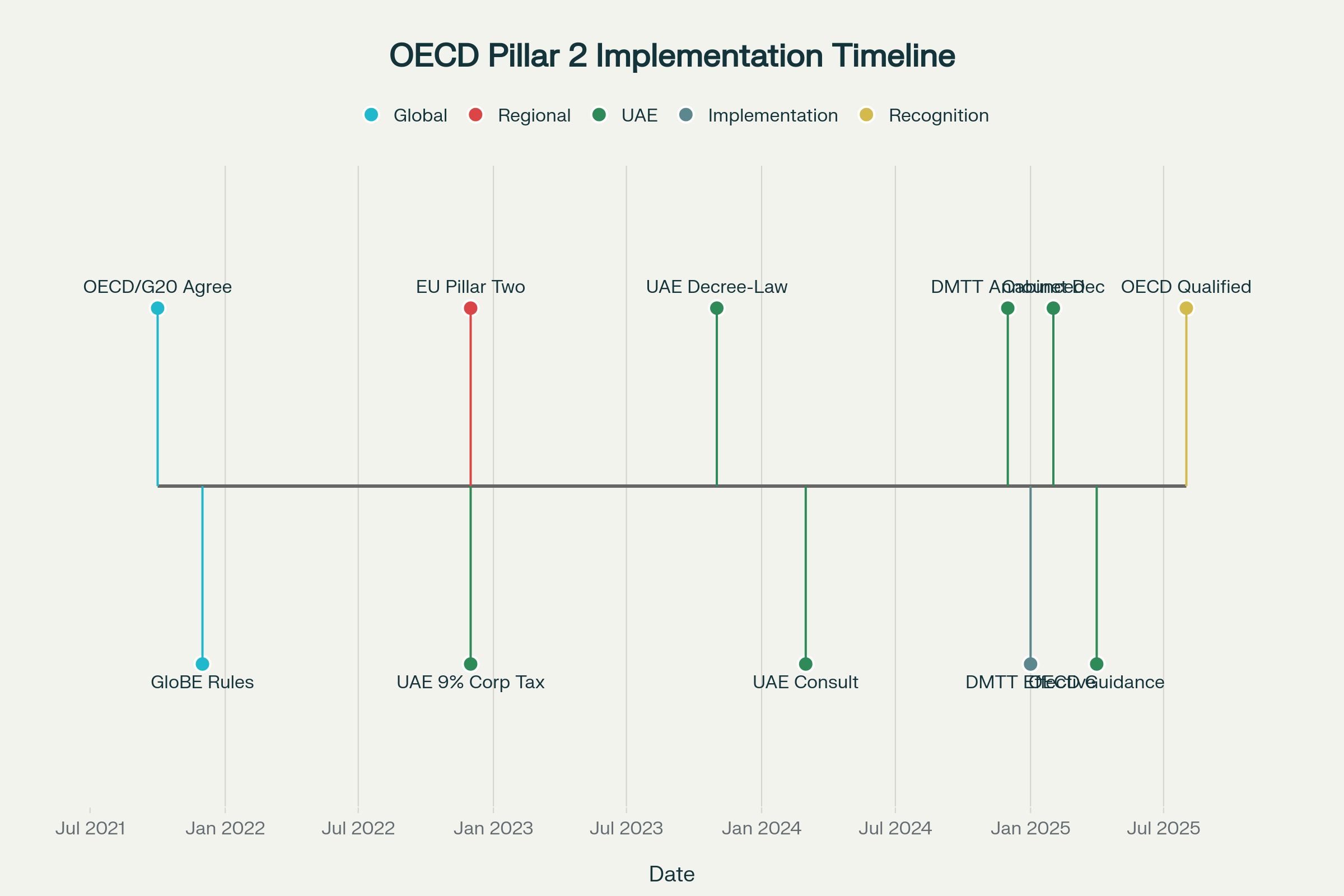

From 1 January 2025, the UAE applies a 15% Domestic Minimum Top‑Up Tax to multinational groups with consolidated revenues above €750 million, aligning with OECD Pillar Two

The UAE has officially entered the global minimum tax era. Starting January 1, 2025, the Emirates implemented a 15% Domestic Minimum Top-Up Tax (DMTT) that fundamentally changes how large multinational enterprises approach their UAE operations. This isn't just another tax policy adjustment – it's a strategic move that positions the UAE as a compliant, forward-thinking business hub while maintaining its competitive edge in the global marketplace.

Here's what this really means for your business: if you're part of a multinational group with consolidated revenues exceeding €750 million in at least two of the past four financial years, you're now subject to this new minimum tax regime. The UAE has essentially said, "We want to keep your business here, but we're playing by global rules now."

The Real Impact on European Companies Operating in UAE

European businesses have long viewed the UAE as a strategic gateway to Middle Eastern and Asian markets, often benefiting from favorable tax structures in free zones and mainland operations. The new DMTT doesn't eliminate these advantages entirely, but it does require a more sophisticated approach to tax planning.

What's particularly interesting is how this aligns with European implementation of similar Pillar 2 rules. Most EU countries have already adopted their own versions of the global minimum tax, creating a more level playing field between European headquarters and UAE subsidiaries. This coordination means European companies can no longer rely solely on jurisdictional arbitrage for tax efficiency.

The UAE's approach includes several practical considerations for European MNEs. The transitional safe harbor provisions offer breathing room through 2026, allowing companies to use simplified calculations if they meet certain thresholds. For instance, if your simplified effective tax rate calculation shows at least 15% in 2024, 16% in 2025, or 17% in 2026, no top-up tax applies.

Recent Updates That Matter

The OECD granted the UAE's DMTT "transitional qualified status" in August 2025, which provides crucial certainty for multinational groups. This recognition means other countries will accept UAE's top-up tax calculations, reducing the risk of double taxation and complex audit disputes. It's the kind of regulatory recognition that makes CFOs sleep better at night.

The UAE also retroactively incorporated OECD administrative guidance from April 2024, June 2024, and January 2025, ensuring their rules stay current with international standards. This proactive approach demonstrates the Emirates' commitment to maintaining alignment with global best practices rather than just meeting minimum requirements.

One significant development involves the UAE's decision to focus initially on DMTT implementation while deferring the Income Inclusion Rule (IIR) and Undertaxed Profits Rule (UTPR). This phased approach gives companies time to adapt their compliance systems without overwhelming administrative burden.

Practical Compliance Challenges and Opportunities

The compliance requirements are substantial but manageable with proper planning. UAE entities must register with the Federal Tax Authority and submit detailed returns within 15 months of the financial year end (18 months for the first transitional year). The calculations involve complex jurisdictional effective tax rate assessments that often require new data collection processes and system upgrades.

Here's where strategic planning becomes crucial. Companies need to evaluate their entire UAE structure – mainland entities, free zone operations, and permanent establishments all fall under the scope if they're part of a qualifying MNE group. The traditional benefits of UAE free zones remain for smaller businesses and those outside the €750 million threshold, but large MNEs need a more nuanced approach.

The reporting requirements align with the Global Anti-Base Erosion (GloBE) information return standards, creating consistency across jurisdictions implementing Pillar 2. This standardization actually helps multinational groups streamline their global compliance processes rather than managing completely different requirements in each country.

Strategic Considerations for Tax Advisory Services

Professional service providers are seeing increased demand for comprehensive Pillar 2 readiness assessments. The most effective approach combines technical tax analysis with operational business review, examining how the new rules interact with existing UAE corporate tax obligations, VAT requirements, and transfer pricing documentation.

The key insight is that DMTT compliance isn't just about calculating and paying additional tax. It's about optimizing global tax positions while ensuring substance requirements are met. Many companies are discovering opportunities to rationalize their UAE operations, potentially consolidating entities or restructuring intercompany arrangements to achieve better overall tax efficiency.

European clients particularly benefit from coordinated planning that considers both UAE DMTT obligations and European Pillar 2 implementations. The timing differences between jurisdictions create planning opportunities for companies willing to take a comprehensive approach rather than treating each country's requirements in isolation.

Economic Impact and Future Outlook

The OECD estimates that global minimum tax rules will generate $155-192 billion annually worldwide, representing 6.5-8.1% of current global corporate income tax revenues. For the UAE, this represents a significant diversification of government revenue beyond oil-related income, supporting the country's long-term economic vision.

What makes the UAE's implementation particularly effective is the balance between compliance and competitiveness. The country maintains numerous incentives for qualifying activities, including research and development tax credits of 30-50% starting in January 2026, and high-income employment credits effective from January 2025. These incentives help offset the impact of higher minimum tax rates for companies engaged in substantive economic activities.

The global trend is clear: approximately 90% of multinational companies in scope of Pillar 2 rules will be subject to 15% minimum tax by 2025. Countries that implement comprehensive, business-friendly versions of these rules early are positioning themselves advantageously for continued foreign investment.

Making Sense of the New Reality

The UAE's implementation of OECD Pillar 2 represents a maturation of its tax policy rather than a retreat from business-friendly practices. Companies that embrace this new framework and plan accordingly will find the UAE remains an attractive destination for regional headquarters, treasury centers, and operational hubs.

The key is moving beyond viewing this as simply a new cost of doing business. Smart companies are using Pillar 2 implementation as an opportunity to optimize their overall tax positions, improve operational efficiency, and demonstrate commitment to responsible tax practices that resonate with stakeholders.

For multinational enterprises, particularly those with European connections, the UAE's approach to OECD Pillar 2 offers predictability and alignment with global standards. The combination of clear implementation timelines, practical safe harbor provisions, and ongoing incentives for substantive business activities creates a framework that supports continued growth while meeting international compliance expectations.

The message is straightforward: the UAE has successfully navigated the transition to global minimum tax compliance while preserving its fundamental attractiveness as a business destination. Companies that understand and adapt to this new environment will be well-positioned for continued success in one of the world's most dynamic business hubs.

.jpg)

.jpg)