What Are the Compliances a Company Must Follow in India? (AGM, ROC Filings, Audit & More)

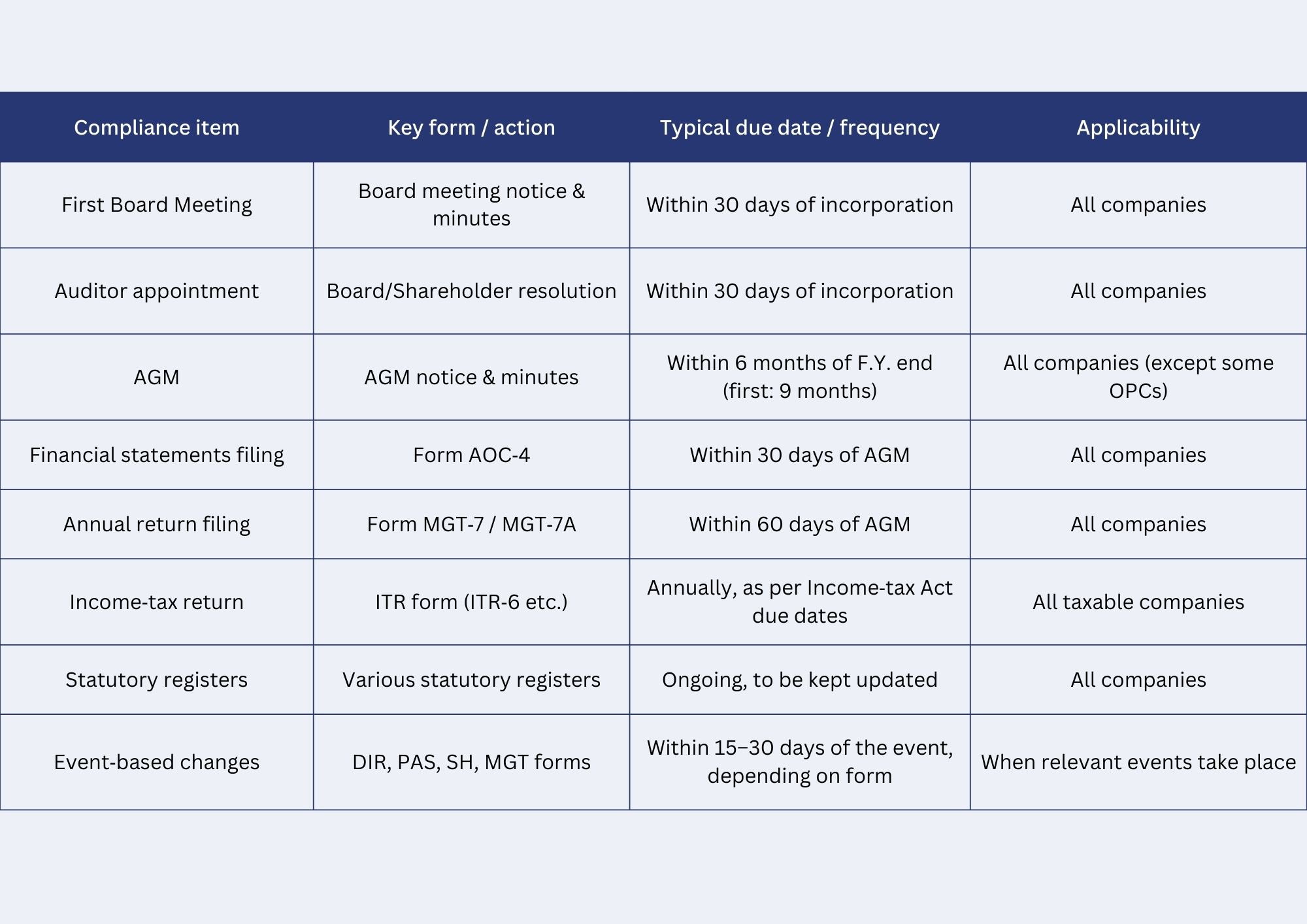

After incorporation, every Indian company must follow ongoing compliances such as Board Meetings, Annual General Meetings, audited financial statements, annual return filing with the RoC, and maintenance of statutory registers. It must also comply with event‑based filings for changes in directors, capital or registered office, and meet all tax and licence obligations. Staying updated with these legal requirements helps avoid penalties, preserves active company status, and supports smooth business operations.

.jpg)

A company registered in India must comply with ongoing corporate law, tax, and regulatory requirements to stay legally active and avoid penalties. These compliances start immediately after incorporation and continue annually throughout the life of the company.

Core post‑incorporation compliances

- Hold the first Board Meeting within 30 days of incorporation and at least four Board Meetings every year with a maximum gap of 120 days between two meetings.

- Verify the registered office and file the relevant form with the Registrar of Companies (RoC) within the prescribed time.

- Appoint the first auditor within 30 days of incorporation at the Board Meeting; if the Board fails, shareholders appoint in a General Meeting.

- Issue share certificates to subscribers within 60 days from the date of incorporation and record them in the statutory registers.

Annual corporate compliances (Companies Act, 2013)

- Annual General Meeting (AGM): Hold an AGM within six months from the end of every financial year; the first AGM must be held within nine months from the end of the first financial year.

- Financial Statements (AOC‑4): File audited financial statements (Balance Sheet, Profit & Loss, Cash Flow Statement, notes, auditor’s report) in Form AOC‑4 within 30 days of the AGM with the RoC.

- Annual Return (MGT‑7 / MGT‑7A): File the annual return within 60 days of the AGM, capturing shareholding pattern, directors, and key corporate information.

- Statutory Registers: Maintain updated registers such as Register of Members, Register of Directors and KMP, Register of Charges, and Register of Contracts or Arrangements in which directors are interested.

Board, audit and records related compliances

- Conduct a statutory audit every year by a qualified Chartered Accountant, and ensure the auditor’s appointment/ratification as per the Companies Act.

- Prepare minutes of all Board and General Meetings within the prescribed time and maintain them at the registered office.

- Maintain proper books of account and vouchers at the registered office (or any other notified place) in accordance with the Act and applicable accounting standards.

Event‑based & allied regulatory compliances

- Obtain and maintain registrations like GST, Professional Tax, Shops & Establishments, and industry‑specific licenses, wherever applicable.

- File necessary forms for changes such as appointment/resignation of directors, change in registered office, increase in authorised share capital, and allotment or transfer of shares within prescribed timelines.

- Comply with Income Tax requirements: PAN, TAN, timely TDS/TCS deduction and deposit, advance tax, and filing of income‑tax returns every year.

MCA 2023 company registration snapshot (India)

The data you shared on “Companies Registered in India in 2023 so far” aligns with Ministry of Corporate Affairs statistics where states like Maharashtra, Uttar Pradesh, Delhi, Gujarat, and Karnataka show the highest number of new entities. This mix of LLPs, OPCs, private, and public companies highlights why consistent post‑incorporation and annual compliances are critical to maintaining active legal status across such a large corporate base.

.jpg)